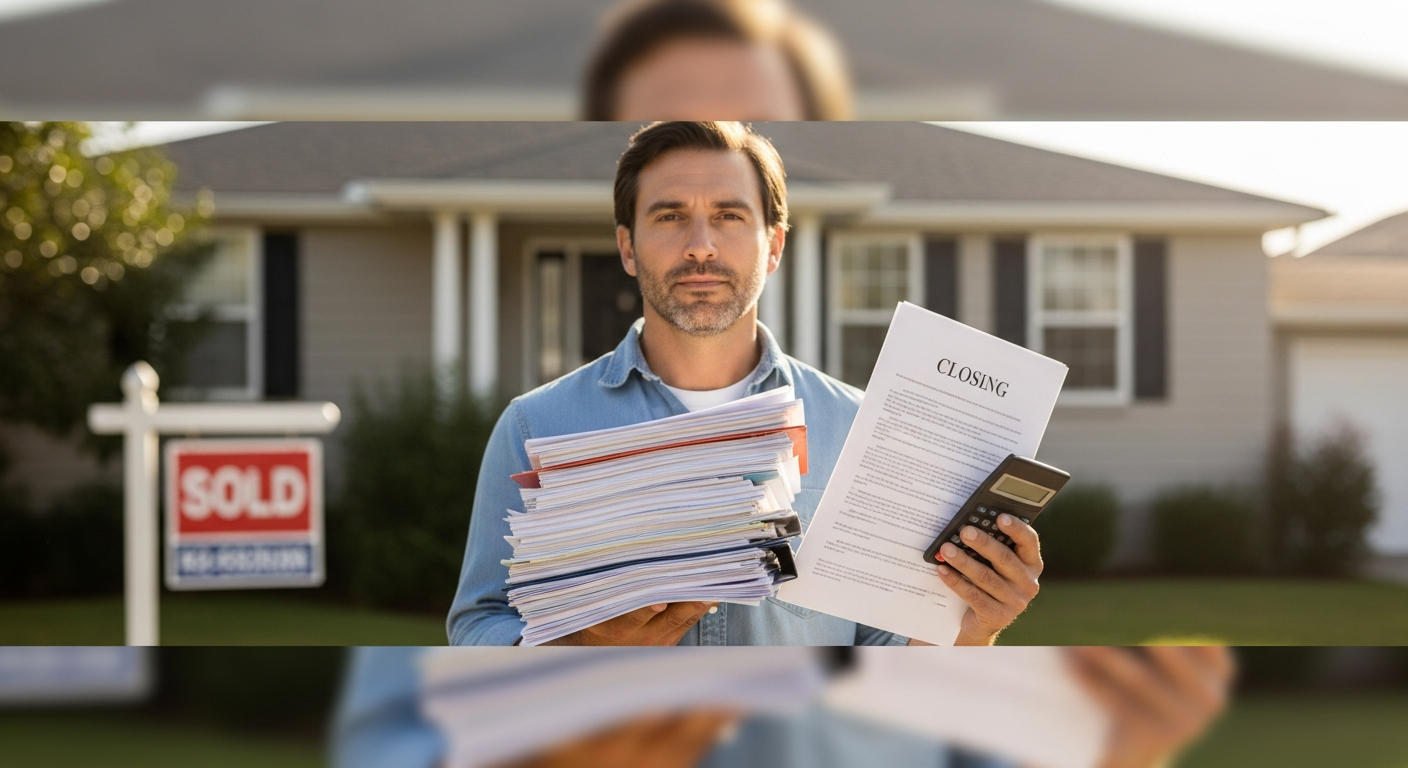

When you decide to sell your home, it's easy to focus on the sale price, but understanding the various costs involved is crucial for an accurate financial picture. Sellers, just like buyers, incur a range of fees at closing. It’s important to distinguish between what are strictly "closing costs" and the "total cost to sell," as many sellers underestimate the latter. While seller closing costs typically fall in the range of 1% to 3% of the sale price, this figure doesn't include significant expenses like real estate agent compensation. Once you factor in agent fees, potential repairs, moving expenses and other selling-related costs, the total amount you spend can be considerably higher.

Let's break down the specific fees that typically fall under seller closing costs. First, there are transfer taxes and various local fees. These taxes, calculated as a percentage of the sale price or property value, can vary significantly by location, ranging from 0.5% to 2% in some areas, while others might have a flat fee or no tax at all. For instance, selling a home in Providence, Rhode Island, would likely involve transfer tax, whereas Texas doesn't impose a state transfer tax, though local fees might still apply. Beyond transfer taxes, local governments might require certification or inspection fees, usually ranging from $100 to $500. It's always wise to consult with a real estate agent or title company to understand these location-specific charges.

Next, you'll encounter escrow, title, and recording fees, which are essential for facilitating the property transfer. Escrow fees are charged by the company managing the transaction, with who pays often depending on local custom. Title search fees cover the necessary research to confirm clear ownership and check for any liens. Recording fees are paid to the local government to officially document the transfer of ownership. These administrative fees typically range from $200 to $1,900, depending on the jurisdiction and transaction complexity.

Another common seller expense is owner’s title insurance, which protects the buyer against future ownership claims or title defects. The average cost for this insurance is about 0.67% of the purchase price, though total title-related fees can vary. In many states, sellers traditionally cover this cost, but again, local customs and negotiations can influence who ultimately pays.

Sellers are also responsible for prorated property taxes and utilities up to the closing date. If the sale occurs mid-year, property taxes will be prorated so you only pay for the period you owned the home. Similarly, utility bills like water, electricity, and gas may be prorated. These expenses can range from a few hundred to several thousand dollars, depending on local tax rates and the specific closing date.

Finally, if your home is part of a homeowners association, you might face additional HOA-related fees at closing. These can include transfer fees, resale package fees, estoppel fees, and prorated HOA dues. In some situations, sellers might also be responsible for any unpaid HOA dues or special assessments approved before the sale. Because these costs vary widely by community, reviewing your HOA documents and discussing them with your real estate agent is a good step.

Beyond these direct closing costs, several other major expenses significantly impact your net proceeds. Real estate agent compensation, while not technically a closing cost, is often the largest single expense for sellers and is typically negotiable. Seller concessions, which can be 3% to 6% of the sale price, are negotiated with the buyer and directly reduce your take-home amount. Other costs include repairs and renovations made before listing, home staging, professional photography and listing preparation, moving expenses and carrying costs like mortgage payments and utilities while the home is on the market. Of course, the payoff of your existing mortgage is also a major deduction from the sale proceeds.

Many sellers focus solely on the 1-3% closing cost estimate and fail to account for these broader selling expenses, leading to an inaccurate expectation of their final profit. Understanding the full scope of costs, both direct closing fees and other selling expenses, is essential for truly knowing what you'll walk away with after the sale.

I think what stands out here is just how many different pieces contribute to the final cost of selling a home. It’s easy to get caught up in the sale price, but truly understanding these various fees and expenses upfront can make a huge difference in your financial planning and overall experience.

Seller Costs: What You Really Pay

4 min read·Jun 8, 2026Neet help with buying / selling process?

Serviing the New River Valley Area

Mortgage rates just surged to their highest point this year, marking four straight weeks of increases. This jump to 6.66% is directly tied to global events, making it crucial for anyone eyeing the housing market.

The housing market is shifting, offering new opportunities for buyers as conditions rebalance. Recent data shows a notable uptick in both home prices and available inventory.

Major universities are facing a significant drop in graduate student enrollment, a trend with ripple effects far beyond campus. This shift could reshape local rental markets and community dynamics in university towns.

Finding the right tenant in Blacksburg's unique market is crucial for your rental success. A thorough screening process can safeguard your investment, ensuring consistent income and a stable experience.

Setting the right rental price in Blacksburg is crucial, but many owners miss the mark. Learn how strategic pricing can fill your vacancies faster and boost your bottom line.

National home prices are cooling, but that's just an average. Dive into local markets, and you'll find a wildly different story playing out, all driven by one crucial factor.